Monthly Summary – November 2021

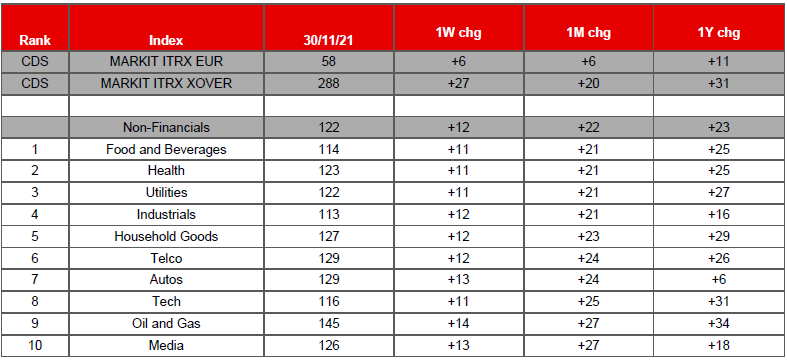

November brought back volatility to markets as concerns over Omicron surfaced on the eve of Thanksgiving, low market liquidity amplified moves as the Vix index jumped sharply briefly spiking above 28. Synthetic indices spiked wider on the month with Main +6bps wider at 58bps and XO +20bps wider at 288bps. Rates rallied on the back of concerns about the new virus strand with the 10 Bund yield down to -0.33% which is -16bps lower on the month and UST 10 year -10bps to 1.45%. In the UK we saw 10 year Gilts back below 1% at 0.81% at month end which was -20bps on the month.

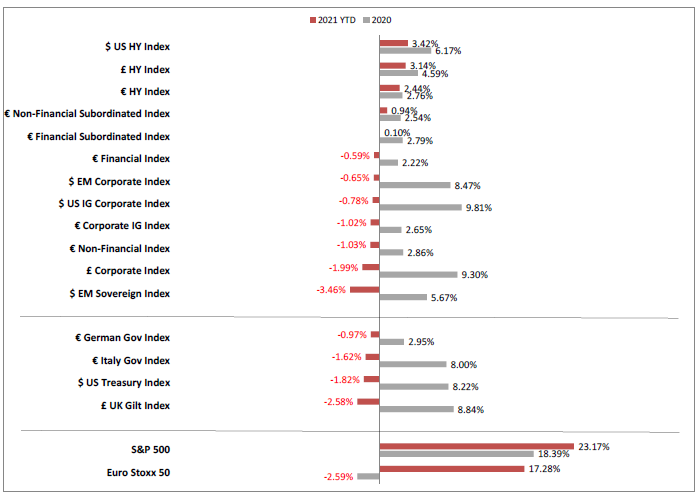

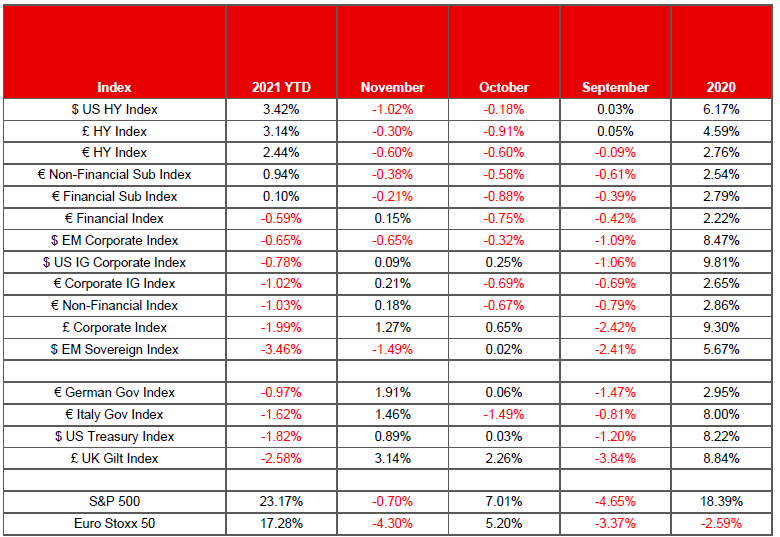

New issue senior volumes continued their momentum with €22bn in seniors and €3.5bn in corporate hybrids pricing on the month, and we saw both Euro and US Dollar denominated issuance in the sub space. Total returns for November were broadly negative with only the rates rally offsetting widening credit spreads; EM and HY indices fared the worst but HY and subordinated indices are still black on a YTD basis. Sterling corporates bounced back in November thanks to the rates move and less issuance and are now at -1.99% on a YTD basis.

CHART 1: ASSET CLASS TOTAL RETURN PERFORMANCE SUMMARY

Source: Bloomberg, ICE BofAML, MUFG

CHART 2: ASSET CLASS TOTAL RETURN PERFORMANCE

Source: Bloomberg, ICE BofAML, MUFG

Unsurprisingly the risk off tone in November impacted returns for the month with only the rates rally helping offset the months credit spread widening. The biggest monthly losers were the EM $ Sovereign index which was -1.49% and US $ HY which was -1.02%, HY together with subordinated indices lagged the space most but at the other end of the spectrum £ Corporates finished the month +1.27% thanks to the gilt rally and its longer duration nature.

Senior indices just managed to scrape the month into the black with € Non-Financial Index finishing the month was +0.09% and € Financial Index +0.15%, which meant that on a YTD basis they are -0.78% and -0.59% respectively. While Euro IG subordinate indices followed HY and performed negatively over the month, with € Non-Financial Subordinate Index down -0.38% and € Financial Subordinate Index at -0.21% which leaves YTD performance at +0.94% and +0.10% respectively.

CHART 3: CDS AND IBOXX SECTOR Z SPREAD PERFORMANCE BY 1M CHANGE

Source: IHS Markit, MUFG, Bloomberg

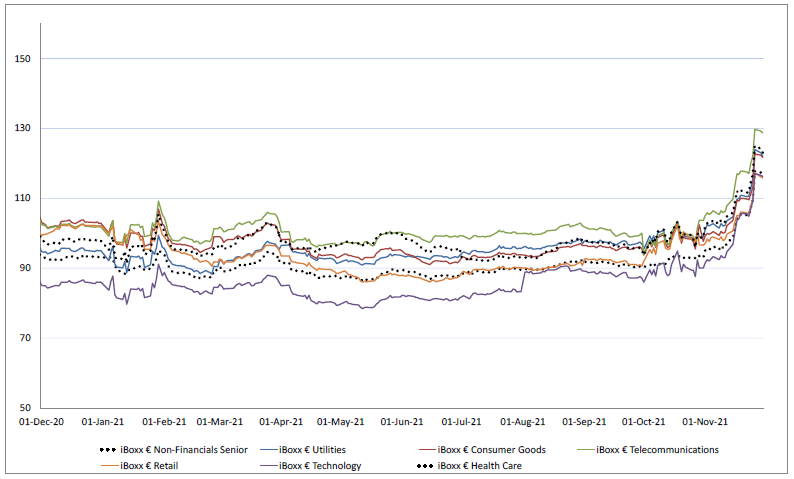

CHART 4: IBOXX SECTOR PERFORMANCE- LOW BETA

Source: IHS Markit, MUFG

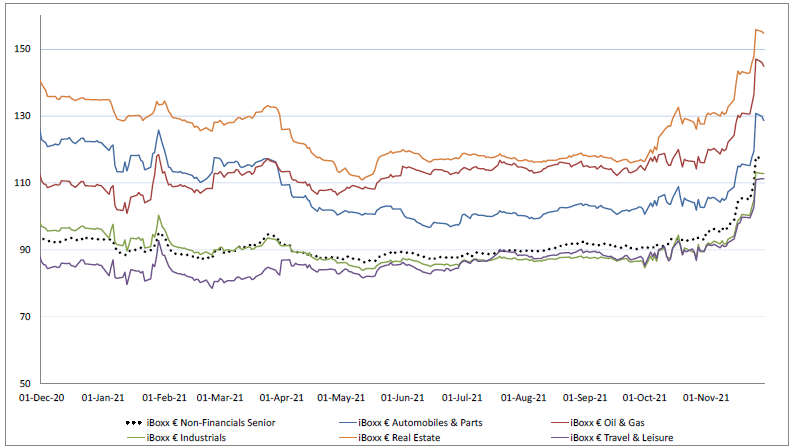

CHART 5: IBOXX SECTOR PERFORMANCE- HIGH BETA

Source: IHS Markit, MUFG

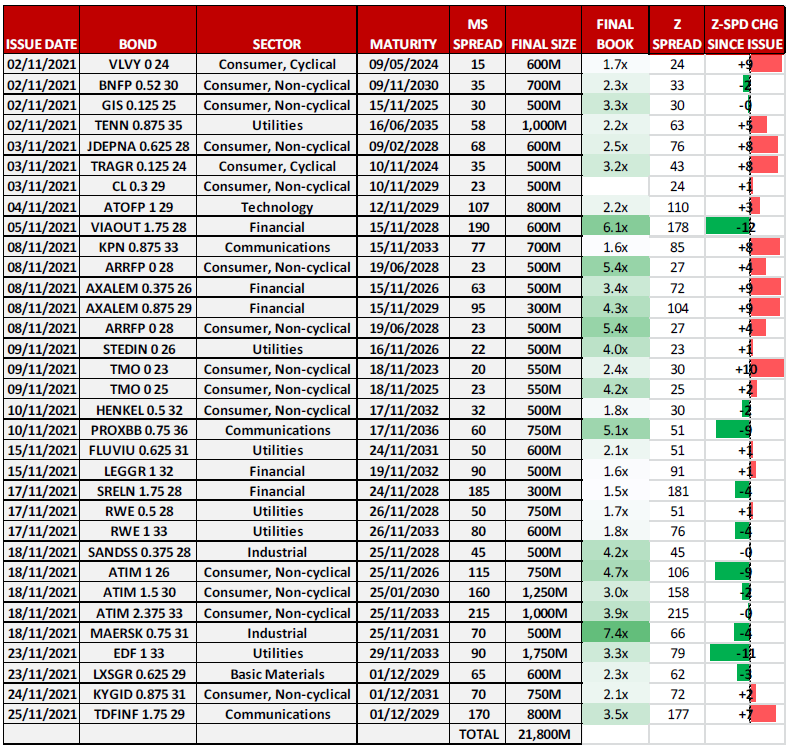

November’s new issue momentum continued on from a solid October with over €21.8bn issued across senior euro corporate issuance and a further €3.5bn across corporate hybrids.

Within the senior corporate space we saw a flurry of activity in the first part of the month, there wasn’t many multi-tranche deals coming to the market except ASTM the Italian toll road operator pricing a three part deal, with most deals being one tranche offerings and a whole host of names including AA rated Colgate printing a 8 year deal at MS+23 to an inaugural deal from Via Outlets the BBB- rated real estate name that issued a green bond at MS+190 for a 7 year.

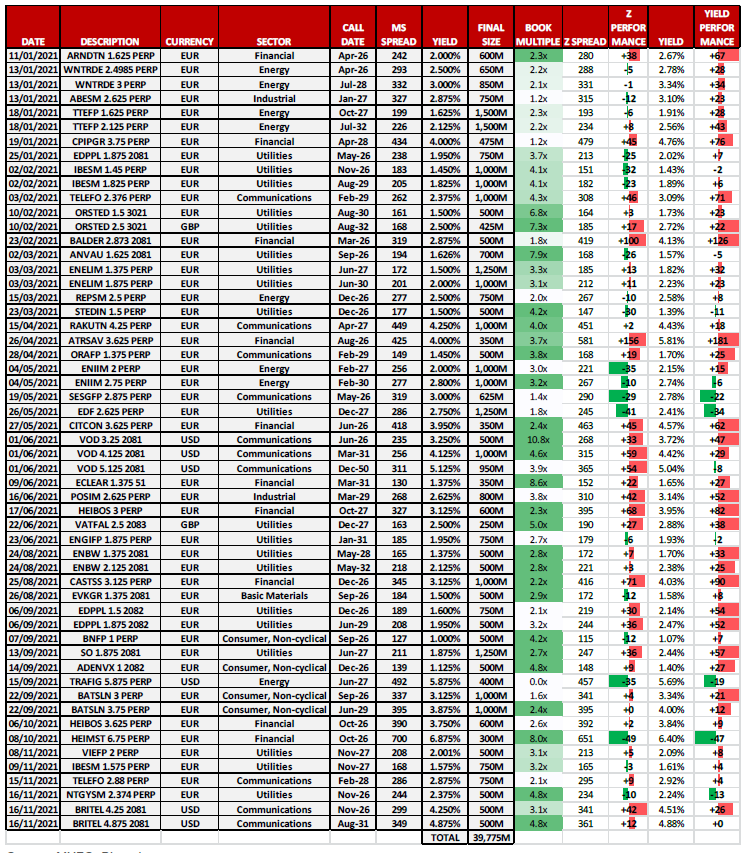

Euro denominated hybrid issuance all came from established issuers as we saw Veolia, Iberdrola, Naturgy and Telefonica all print benchmark deals, ESG structures remained popular as ever with the Iberdrola being structured as a green bond and Telefonica as sustainable. BT made a surprise appearance in the USD market with a dual tranche in the middle on the month, the company priced a NC5.25 and NC10 at attractive levels of 4.25% and 5% respectively, the new bonds came with a change of control to ease concerns about any potential takeover from Patrick Draghi.

CHART 6: MONTHLY SENIOR EURO IG NEW ISSUANCE SUMMARY

Source: MUFG, Bloomberg

CHART 7: HYBRID ISSUANCE SUMMARY 2021

Source: MUFG, Bloomberg

The heavy tone of the market meant that underperformers dominated our lists with some bonds moving +40-50bps wider in short order. Omicron concerns hurt travel related issuers most with EasyJet, Ryanair, Wizz and Aeroports de Paris all materially wider on the month as the most exposed names traded lower.

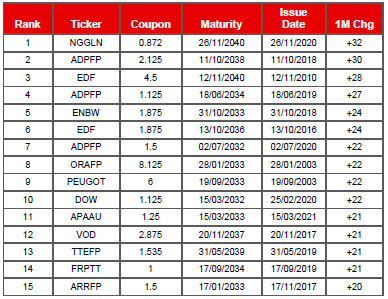

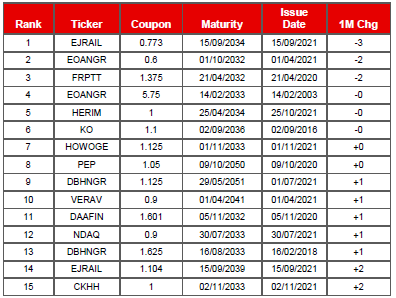

In terms of bonds that traded better on the month Syngenta outperformed on strong results and an upgrade to BBB from S&P, but other than that we only had a handful of bonds that traded tighter on the month, those that did included some green bonds such as the E.ON 2032 and higher rated names such as EJRAIL, FTPTT and GEWWOH.

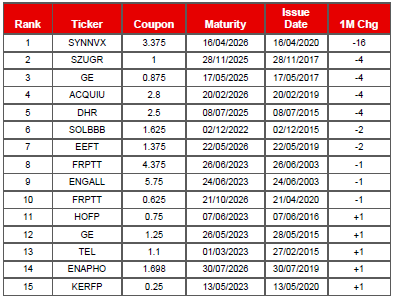

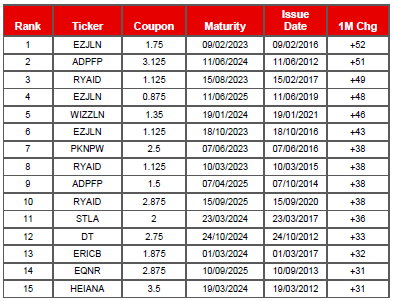

CHART 8: 1-5Y BUCKET BEST PERFORMING BONDS

CHART 9: 1-5Y BUCKET WORST PERFORMING BONDS

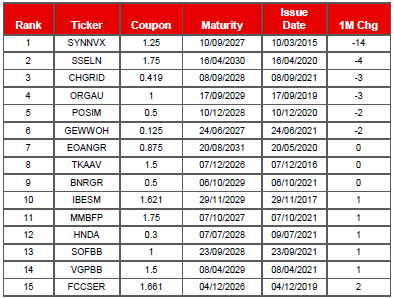

CHART 10: 5-10Y BUCKET BEST PERFORMING BONDS

CHART 11: 5-10Y BUCKET WORST PERFORMING BONDS

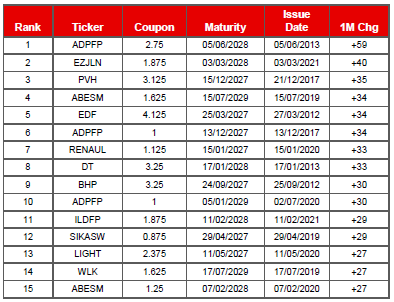

CHART 12: 10Y+ BUCKET BEST PERFORMING BONDS

CHART 13: 10Y+ BUCKET WORST PERFORMING BONDS