- Singapore’s benign inflation could remain entrenched, giving MAS room to ease policy further, possibly as early as at the October meeting, when we anticipate the tariff impact on growth to emerge. We forecast core inflation at 0.6% in 2025 and 1% in 2026.

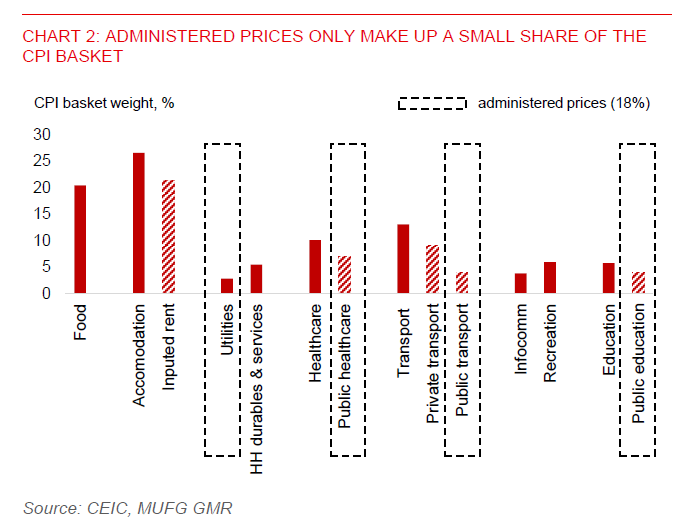

- Government subsidies and rebates will help contain cost pressures, but administered prices account for only ~18% of the CPI basket. Global price dynamics remain a key driver of inflation.

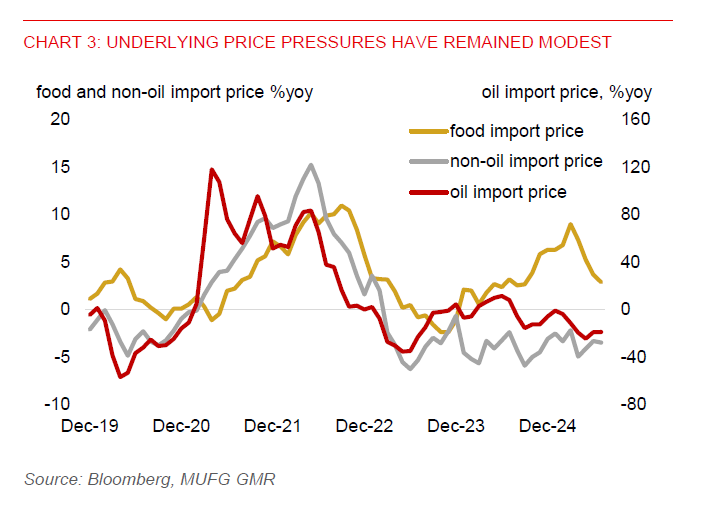

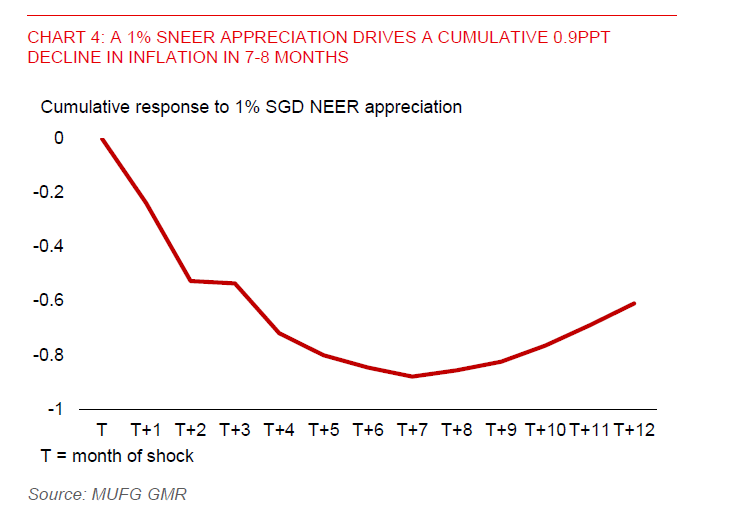

- Easing global commodity prices and a firm Singapore dollar will keep imported inflation in check. A 1% appreciation in Singapore’s nominal effective exchange rate is estimated to reduce core CPI by a cumulative 0.9ppt within 7-8 months.

- Domestic cost pressures will also remain modest, given moderating labour market tightness and falling non-oil import prices. The looming tariff impact will also start to weigh on growth and inflation in Q4 and early 2026

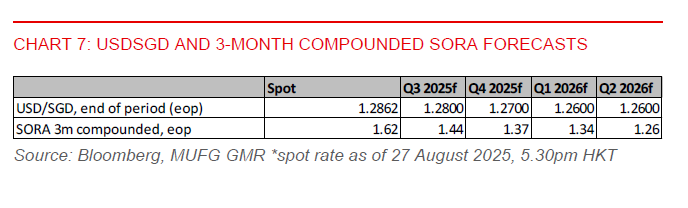

- We forecast USDSGD to fall to 1.2700 by end-2025 and 1.2600 by Q2 2026, mainly due to our expectation for further USD weakness. We also expect the Singapore overnight rate (SORA) to remain soft, amid subdued inflation, a firm SGD, and flush liquidity conditions. We forecast the 3-month compounded SORA to ease to 1.37% by end-2025 and 1.26% in 2026, from 1.60% currently.

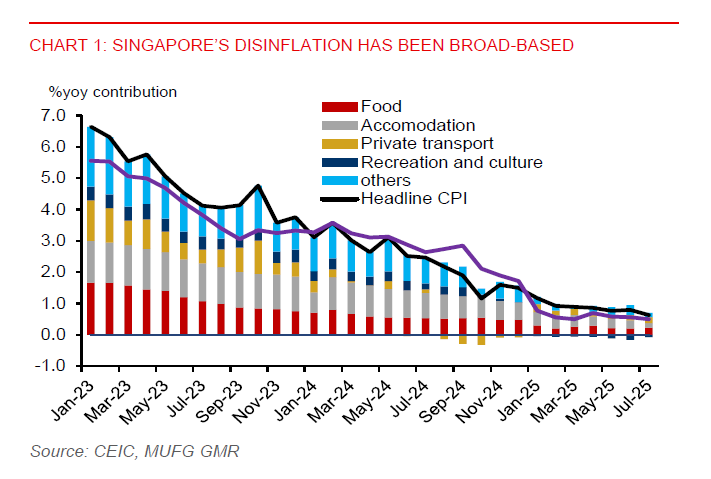

Singapore’s inflation has been subdued this year, with moderation seen in a broad range of goods and services. Headline inflation eased to 0.6%yoy in July, down from 0.8%yoy in Q3, while core inflation (excluding accommodation and private transport) also slowed to 0.5%yoy in July, from 0.6% in Q3. We forecast core inflation to average 0.6% in 2025 and 1% in 2026, reflecting a benign inflation backdrop. This will provide room for the MAS to ease policy further, possibly as soon as at the October policy meeting, especially as we anticipate the tariff impact to emerge in Q4.

STRONG SGD AND SOFTER COMMODITY PRICES SUPPORT DISINFLATION

While the government can play a role to help contain cost of living, global prices will be more crucial to Singapore’s inflation outlook. The Singapore government has introduced several subsidies and rebates to help address the cost-of-living issue and keep prices in check. But it’s notable that administered prices only make up about 18% of the total CPI basket. Moreover, the disinflationary effects of the enhanced healthcare subsidies – introduced in October 2024 – will start to fade.

We expect Singapore’s imported inflation will remained contained this year and next, owing to a moderation in commodity prices and a firm SGD. Softer global growth due to higher US tariffs, coupled with rising OPEC+ crude oil production since Q3 2024, will likely weigh on global crude prices. Brent prices averaged about $70/barrel this year, 12% below the $80/barrel average in 2024. Bloomberg consensus expects Brent prices to ease to $68 this year and $65 in 2026. In addition, the import price of oil fell 18.8%yoy in July, while imported food prices moderated to 2.9%yoy, from 6.3%yoy in March. As a result, Singapore’s food price inflation has slowed to 1.1%yoy in July, versus 2.3%yoy in December 2024.

Our model estimates suggest a 1% appreciation in Singapore’s nominal effective exchange rate (SNEER) will lead to a gradual and persistent drop in core CPI, peaking at around -0.9ppt around 7-8 months after the exchange rate shock. We expect a steady SNEER and broad US dollar weakness to help support SGD, keeping inflation in check.

Local factors are also lending strength to the SGD. A recent 5-year Singapore government bond auction saw robust demand, with the bid-to-cover ratio rising to a one-year high of 2.7, up from 2.5 in May, Singapore’s triple-A credit rating continues to underpin investor confidence, supporting the bond market and, by extension, the SGD. All else equal, a stronger currency would help drive down imported inflation. The disinflationary passthrough of a stronger currency could be sustained via reducing import costs and domestic inflation.

TARIFFS AND FALLING UNIT LABOUR COSTS ARE LIKELY DISINFLATIONARY

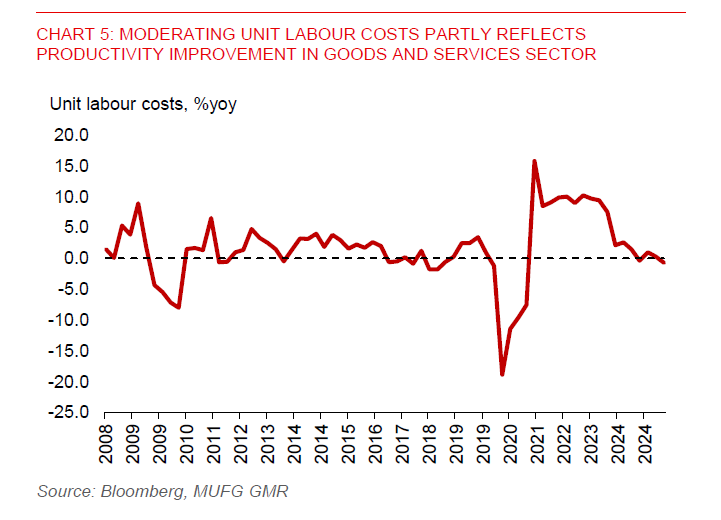

Domestic cost pressures have remained modest. Unit labour costs have been on a broad downtrend, falling by 0.7%yoy in Q2. This was partly underpinned by productivity growth in the goods and services sectors, at 3.3%yoy and 3%yoy in Q2, respectively. In addition, the labour market has become less tight, while the pace of hiring has slowed, which could help keep wage growth in line with productivity gains. Meanwhile, non-oil import prices have also been declining since early 2023, while local prices of goods retained for domestic use have moderated since February.

Looming tariff impact on Singapore’s economy, which could see anaemic growth in H2 compared to a year ago, will also be a drag on inflation. The MAS expects output gap to be around zero this year, reversing the positive gap seen in recent years. We expect the tariff impact to be felt in Q4 and into early 2026. On a year-on-year, Singapore’s NODX fell 4.6%yoy in July, underperforming Bloomberg consensus forecast of a 1%yoy decline. The drag mainly came from non-electronic exports, which fell 6.6%yoy and subtracted 5.2pp from NODX growth. This was slightly offset by electronic exports, which rose 2.8%yoy in July, contributing +0.6pp to NODX growth and marking a 10 straight month of expansion. By destination, exports to the US plunged 42.7%yoy, shipments to China were down by 12.2%, while those to Indonesia fell 32.2%, underscoring weakness in key export markets.

INCREASED COE SUPPLY TO HELP COUNTER RISING PRICES

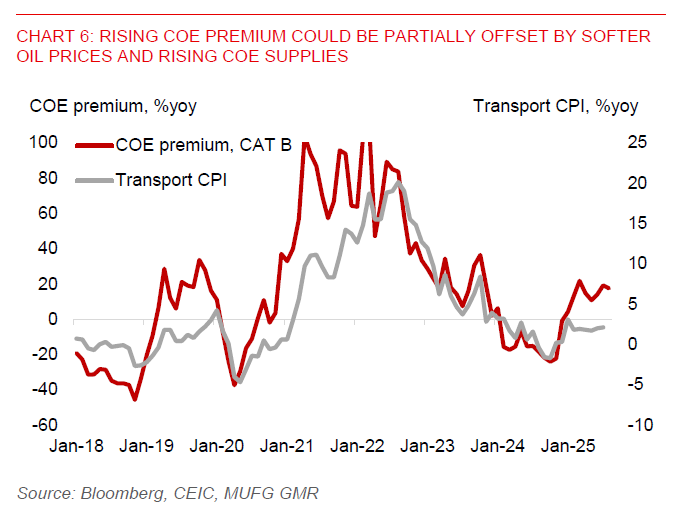

Meanwhile, COE (certificate of entitlement) premiums have increased, but rising supply and softer oil prices will provide an offset. Transport inflation has picked up since the start of the year, rising 2.1%yoy in July. Notably, COE premiums for Category B cars above 1,600cc surged 17.5%yoy to S$124,400 as of 20 August. The government has ramped up the supply of COE to constrain COE price increases, with quotas allocated for Category A, B, and E rising by 25.9%yoy in July.

We forecast the 3-month compounded Singapore overnight rate (SORA) to fall to 1.37% by end-2025 and 1.26% by Q2 2026. Our anticipation for a firm Singapore dollar, subdued inflation, and ample liquidity conditions point to SORA likely remaining soft in the rest of this year. Notably, the 3-month compounded rate has dropped to 1.6%, while SORA has fallen below the 1% level.