Summary

The contrast between the FOMC's unexpectedly hawkish stance and the BOJ's continued easing measures drove the USD/JPY up to 145.90. However, Japanese authorities finally staged a yen-buying intervention stop the yen's slide. The USD has been strengthening overall amid the UK gilt rout, but the USD/JPY remains top-heavy just below 145. The intervention has exerted powerful psychological pressure and had an unexpectedly sustained impact, perhaps because many had doubted that the authorities would actually step into the markets. We think it will be somewhat difficult for the USD/JPY to break past the 1998 high of 147.64 because while Japan does not have a massive amount of funds to deploy for intervention it still has room to take further measures.

September in review

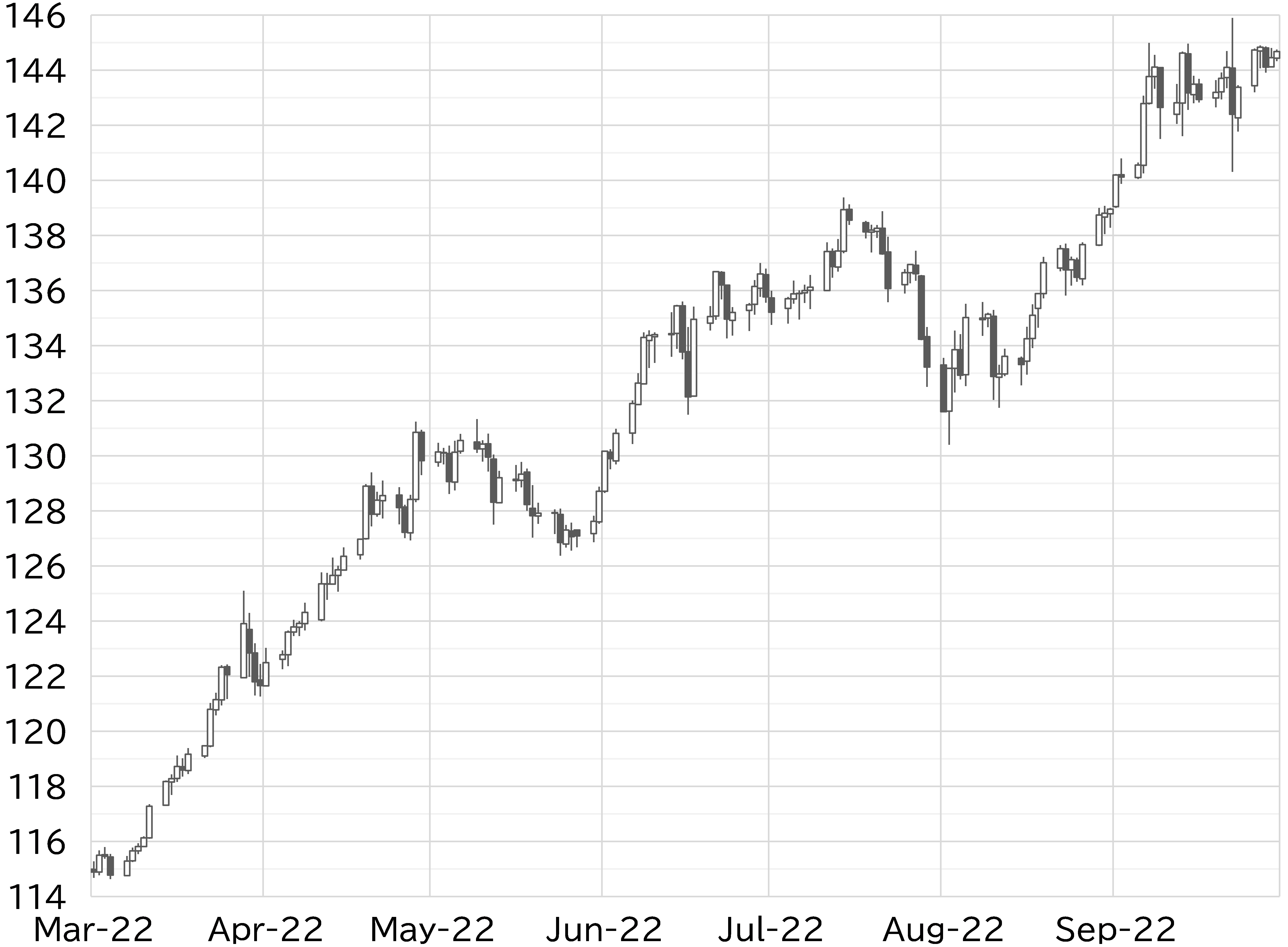

The USD/JPY opened the month at 139.34. It rose to above 140 on 1 September, with the dollar continuing to strengthen following Fed Chair Jerome Powell's speech on 26 August. It remained top-heavy for a while after breaking past this key level but rose swiftly to beyond 142 on 6 September in European trading hours as the yen weakened amid a dearth of catalysts. The dollar strengthened following the stronger than expected US ISM Non-Manufacturing Index released on the same day, driving the USD/JPY to around 143. The pair rose to 144.99 on 7 September after a US newspaper reported that the Fed was likely to raise rates by 75bp at the September FOMC. The psychologically significant watershed of 145 became a ceiling, but the unexpectedly strong US CPI released on 13 September saw the USD/JPY test 145 again on 13–14 September. However, the pair topped out below 145 after the Nikkei reported that the BOJ, which is responsible for executing foreign exchange interventions, had conducted a currency rate check.

The FOMC voted to raise rates by 75bp at its meeting on 21 September as had been expected, but the dot plot showed FOMC members anticipate a higher policy rate than the market had expected. The BOJ maintained its policy settings at the monetary policy meeting on 22 September, and as a result the USD/JPY finally broke past 145. BOJ Governor Haruhiko Kuroda's comments at his press conference stressing that the Bank would maintain its easing stance encouraged the yen to weaken, sending the USD/JPY to 145.90. However, the USD/JPY declined suddenly following the press conference. Soon after that, MOF Vice-Minister of Finance for International Affairs Masato Kanda announced the government would intervene in the currency markets, and the USD/JPY fell back sharply to the mid 140 level. It sank to 140.35 on the same day during US trading hours, but then rallied back to close above 142. The UK government announced a series of tax cuts on 23 September (a public holiday in Japan) which roiled the bond and other financial markets, giving a fresh boost to the dollar, with the USD/JPY rising to above 144.5 by 26 September. The USD/JPY then remained top-heavy below 145 amid concerns of intervention by the Japanese authorities and was trading around the mid 144 level at the time of writing this report (Figure 1).

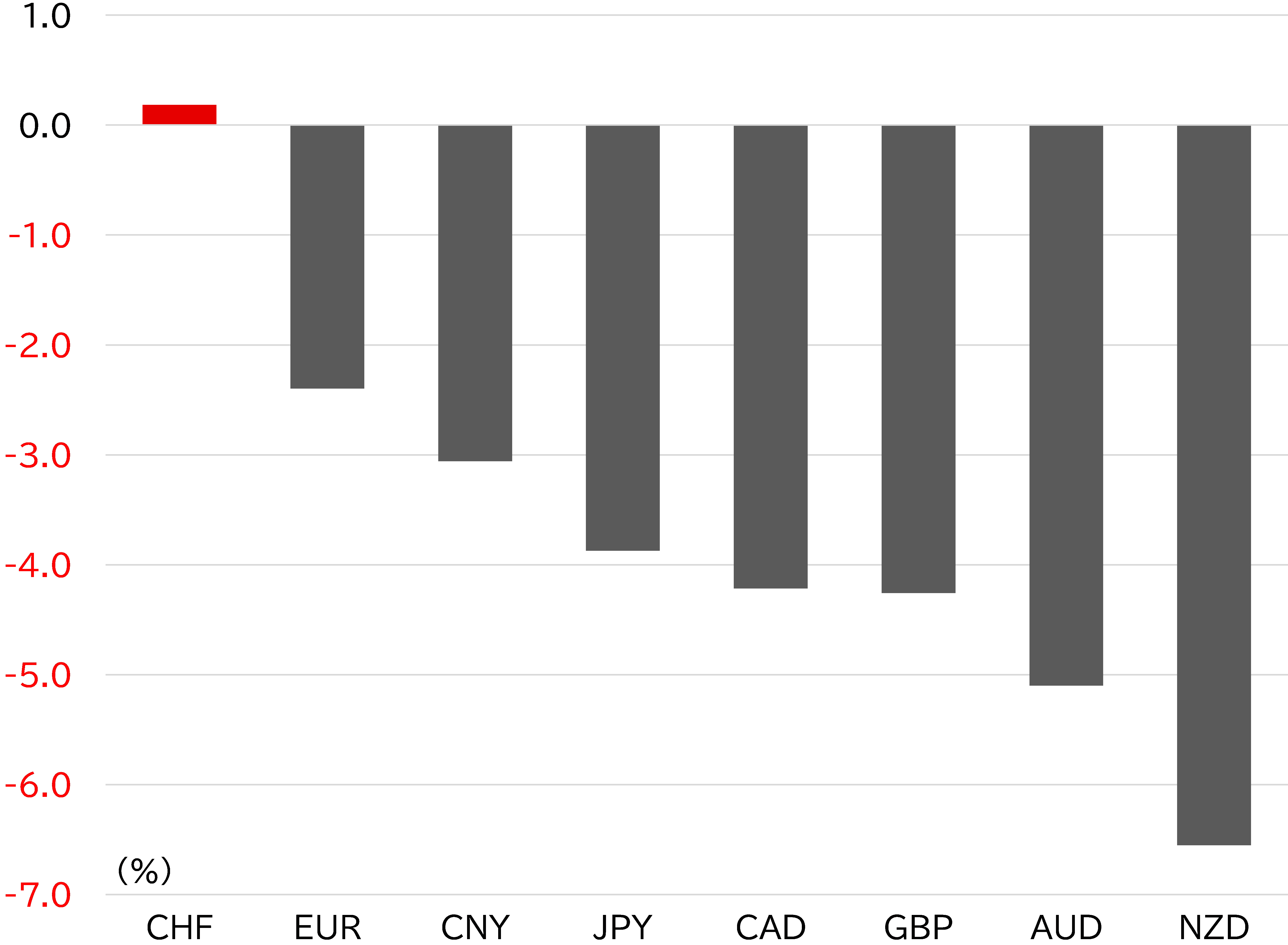

Resource exporter currencies weakened notably in September amid an overall strengthening of the dollar following the FOMC meeting and a decline in oil prices. The sterling rebounded from a record low after the BOE stepped in to buy government bonds, narrowing its margin of decline (Figure 2).

FIGURE 1: USD/JPY (DAILY)

Note: As at 11:00am JST on 30 September

Source: EBS, Refinitiv, MUFG

FIGURE 2: MAJOR CURRENCIES' RATE OF CHANGE VS USD IN SEPTEMBER

Note: As at 11:00am JST on 30 September

Source: Bloomberg, MUFG

First yen-buying intervention in 24 years had some impact

On the evening of 22 September, the MOF announced that it would conduct a yen-buying currency intervention. The rise in the USD/JPY had gained momentum following the FOMC meeting on 21 September, the BOJ's monetary policy meeting on 22 September, and especially around the time of Kuroda's post-meeting press conference. It broke past its most recent high to reach 145.90, then fell back suddenly after 17:00 JST. Shortly after that, MOF’s Kanda announced that the government did intervene in the currency market and the USD/JPY fell by over five yen to 140.40 early in US trading hours. Reports estimate the size of the intervention at JPY2.9–JPY3.6trn based on changes in current account balances at the BOJ. The actual amount will be revealed in the MOF's Foreign Exchange Intervention Operations report released on 30 September at 19:00 JST. Assuming the size of the intervention is in line with reports, it would have been the third largest in yen-denominated terms and the largest ever yen-buying operation (Table 1). However, given that the basic unit of foreign exchange transactions are denominated in dollars, the size of the intervention would come to USD20-25bn at an exchange rate of 145JPY/USD. Japan's largest currency intervention amounted to JPY8.6trn on 31 October 2011, which would come to about USD100bn based on the exchange rate at the time of around 75JPY/USD. The USD/JPY rate fluctuated by up to 3.8% on the day of the recent intervention, compared to about 5.6% on 31 October 2011. Despite the differences in the direction of the operations (yen-buying vs yen-selling), we would have to agree with Finance Minister Shunichi Suzuki's assessment that at least the initial impact of the intervention was effective. In addition, although the USD/JPY subsequently rebounded to just below 145, it has become top-heavy at this level. The USD has strengthened across the board as the turmoil in the bond market due to the UK's tax cut announcement has spread. Despite that, concerns that Japan could intervene again appear to have limited a rise in the USD/JPY. The MOF explained that the intervention was aimed at dealing with rapid market fluctuations (yen depreciation) and was not an attempt to intentionally shift toward a stronger yen. Based on this, we think it is fair to say that the intervention has had a sustained impact (although for less than a week at this point).

We note that when currency intervention involves selling the dollar and buying the yen, the market tends to focus on how much foreign currency is available as a source of funds. Foreign exchange reserves correspond to this, and Japan held USD1.3trn in reserves as of the end of August. Of this amount, about USD1.2trn is foreign currency. Securities accounted for USD1.0368trn and deposits USD136.1bn. Securities are mainly likely to be investments in USTs, but based on materials published in the past, securities with a remaining maturity of less than one year that should be easy to sell due to their high cash ability and liquidity are estimated to account for 14% of holdings. In other words, about USD168bn of securities and USD136.1bn of deposits (totaling about USD300bn) could be considered as funds that could be immediately tapped for interventions. Of course, we cannot be certain of how flexibly securities and cash could be used to finance currency interventions, but considering Japan spent USD25bn at most on 22 September, we think the government still has considerable buying power, although we would not call the war-chest massive. Many people had been skeptical that the government would actually intervene in the currency markets despite the rise in the USD/JPY and Japanese authorities becoming increasingly clear that they would move in response. This means the intervention has already probably had a strong psychological impact. The USD/JPY could rise past 145 again, but we think further catalysts will be needed for it to test the 1998 high of 147.64.

TABLE 1: RESULTS OF INTERVENTIONS BY JAPANESE AUTHORITIES (FIVE WITH LARGE YEN-DENOMINATED AMOUNTS)

(Note) "Exchange rate" is the median price range on the day of intervention; "intraday maximum fluctuation" is the difference between the high and low prices.

Source: MOF, EBS, Refinitiv, MUFG

Hawkish shift in US monetary policy stance nearing its limit

We think the driving force behind the USD/JPY's sharp rise over the last six months has been the Fed's increasingly hawkish monetary policy stance, the accompanying rise in UST yields, especially in the intermediate sector, and the strengthening of the dollar. Yen depreciation due to the sense of divergence in monetary policy in Japan and abroad was fueled by the change in the Fed's stance.

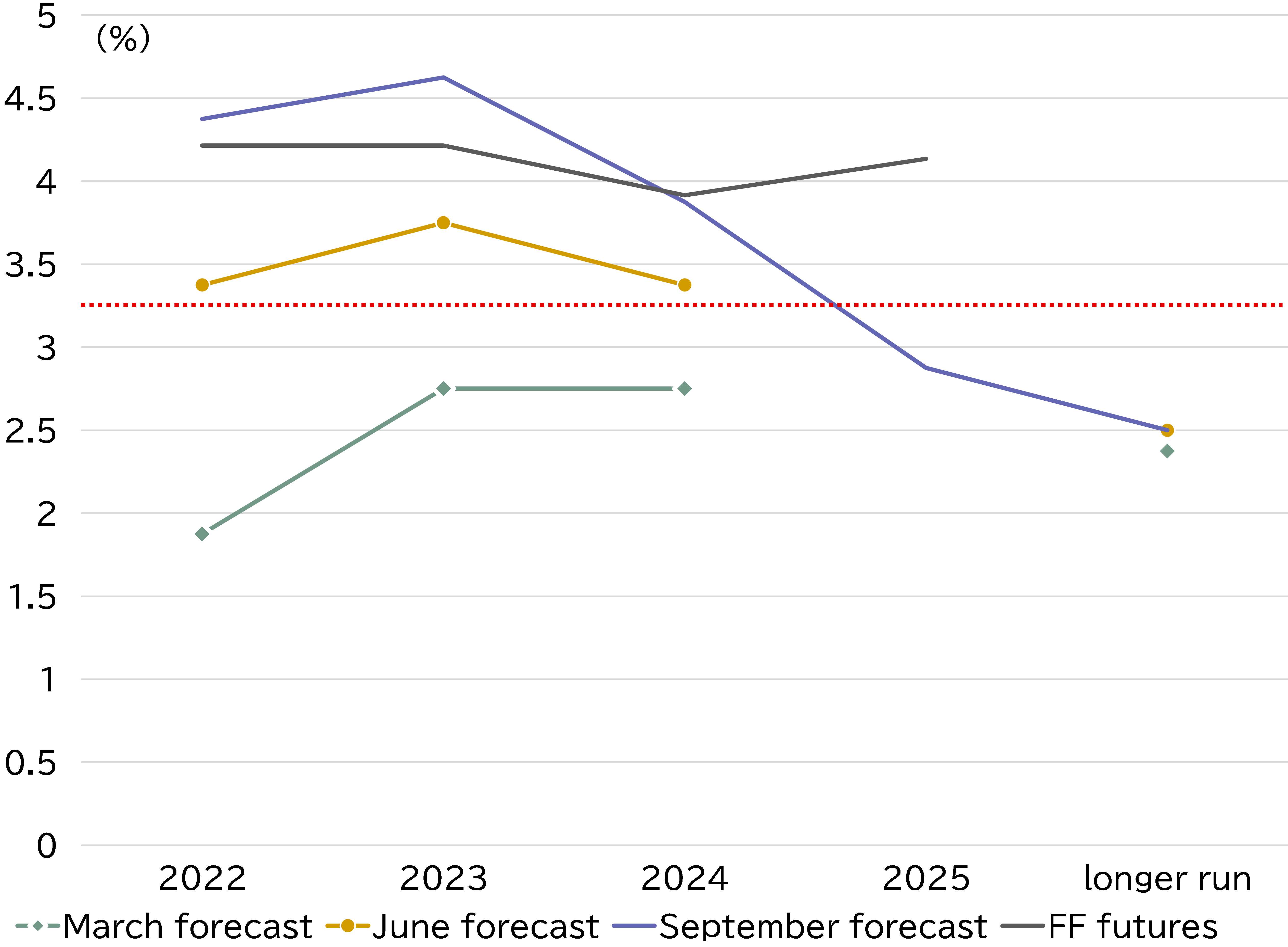

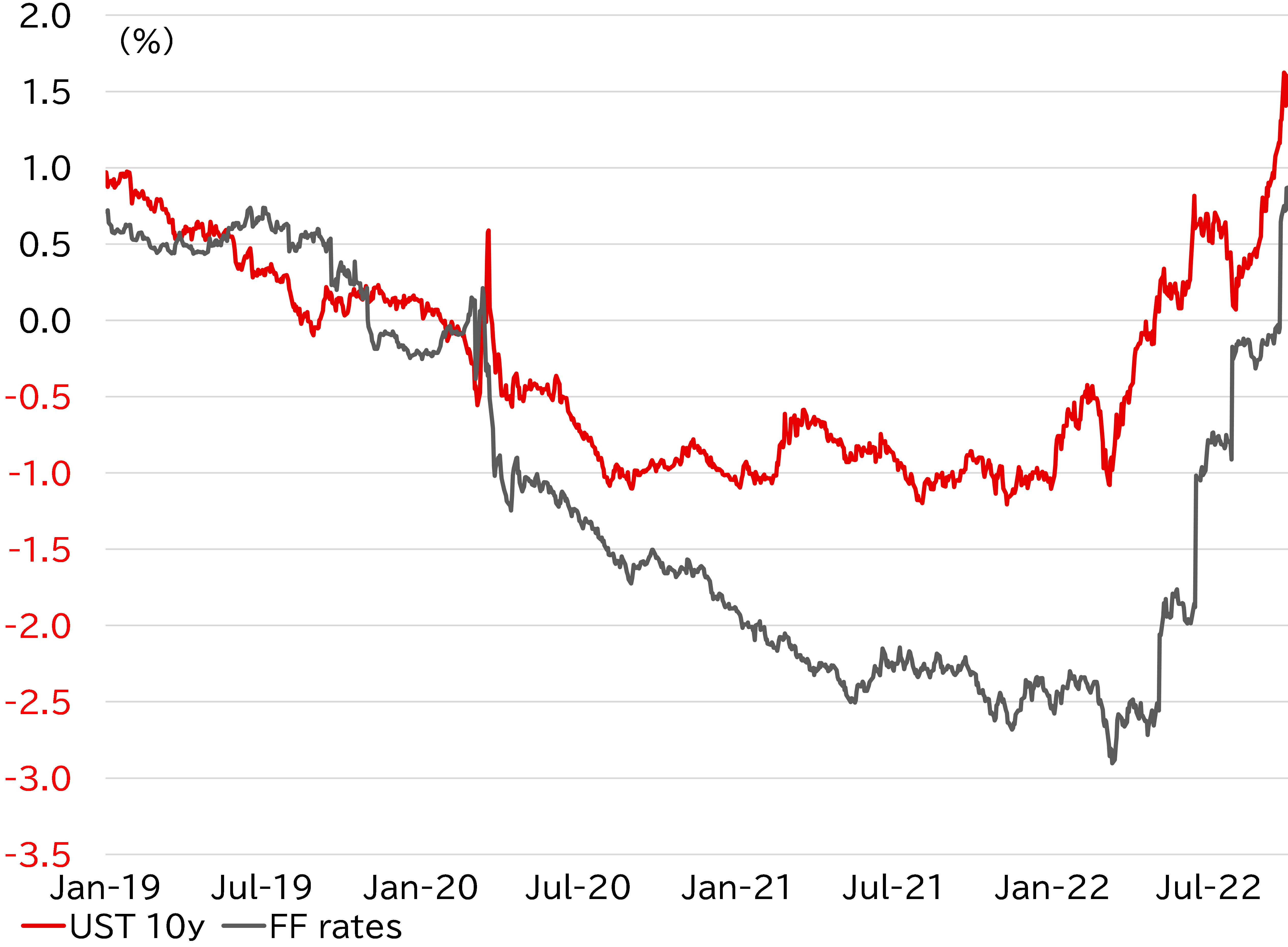

The outlook for policy rates through 2025 presented at the September FOMC meeting was higher than the market had expected (Figure 3). Combined with the UK gilt shock that followed, this resulted in the 2y UST yield temporarily rising past 4.30% and the 10y yield above 4.00%. The outlook for the policy rate shown in the dot plot therefore seems to have been largely factored in. Meanwhile, regional Fed reports have pointed to signs of a slowdown in the US economy and inflation, and leading economic indicators are also trending downward. The labor market remains tight, but higher mortgage rates are softening real estate prices. It appears that the Fed's stance of curbing inflation even if it means dampening the economy has already been put into practice. In addition, the 75bp rate hike in September has pushed the federal funds rate well above the neutral rate of interest, meaning it has entered positive territory even in real terms (Figure 4) and that monetary conditions in the US will tighten in earnest from here. In other words, the slowdown in the US economy looks poised to move into full gear. The Fed has also accelerated the scaling back of its balance sheet since September. These conditions are putting downward pressure on stock prices, with the S&P500 falling to its lowest level since December 2020. However, the Fed looks prepared to accept a further slide in stock prices judging by its current stance.

As noted in last month's report, the Fed's stance of prioritizing efforts to curb inflation, even if this means hurting the economy and stock prices, has been supported by public dissatisfaction with rising prices. Gasoline prices have fallen slightly and supply constraints have been resolved to some extent, but we think the economic slowdown and decline in share prices could ramp up from here given the Fed's rate hikes and balance sheet cut backs point to a phase of fully-fledged monetary tightening. The key question is therefore whether the Fed can maintain its hawkish stance. In the run-up to the mid-term elections in November, the Fed is likely to face increasing pressure to be more mindful of the economy. At the very least, the environment which supported the Fed's increasingly hawkish stance has changed. The Fed is likely to be even more cautious in its dialogue with the market given Powell's comments after the July meeting raised expectations of an early interest rate cut. However, like it or not, the market will be highly focused on changes in the Fed's monetary policy from now through to the end of the year. We suspect that in retrospect the September FOMC meeting will mark the peak of the Fed's hawkish tilt. We also expect the dollar's strength is approaching an apex, although we are not yet certain what the specific trigger will be.

The dollar's strength versus other currencies has gained momentum since the UK gilt rout, but US authorities have been downbeat on taking measures to weaken the dollar. The strong dollar is already putting pressure on the profits of large global companies and traditional domestic manufacturers. Even so, the general consensus that the dollar should be allowed to rise in order to curb imported inflation is unlikely to change. Treasury Secretary Janet Yellen, who was expected to step down after the midterm elections, has also announced that she is willing to remain in office. It is therefore hard to imagine that the US will suddenly shift to an exchange rate policy that approves of a weaker dollar.

FIGURE 3: DOT PLOT MEDIAN FF RATE FORECASTS

Source: Fed, Bloomberg, MUFG

FIGURE 4: US REAL INTEREST RATE

Source: Bloomberg, MUFG

BOJ unlikely to act

Meanwhile, the BOJ in September made no major changes to its monetary policy, which has been a factor behind the yen's weakness. The Japanese authorities have adopted monetary policy settings which seek to weaken the yen domestically, while at the same time pursuing an exchange rate policy to defend its value externally through intervention in the foreign exchange markets. Governor Kuroda defended this as an appropriate policy mix when challenged that the policies of the government and BOJ were inconsistent and contradictory. In addition, at his press conference following the monetary policy meeting, he stated that changes to forward guidance and interest rate hikes (adjustment of the yield curve control policy) would not be necessary for "the time being." When asked how long that meant he went off script and answered that it should be assumed to mean a period of two to three years (this is published in the minutes of the press conference). Kuroda's remarks will not bind the policy decisions of the BOJ executive once he leaves office in April next year, but they suggest the Bank is unlikely to adjust its policy settings or change forward guidance at least while he remains at the helm. We therefore do not expect actions from the BOJ to narrow the divergence in monetary policy between Japan and overseas over the next six months.

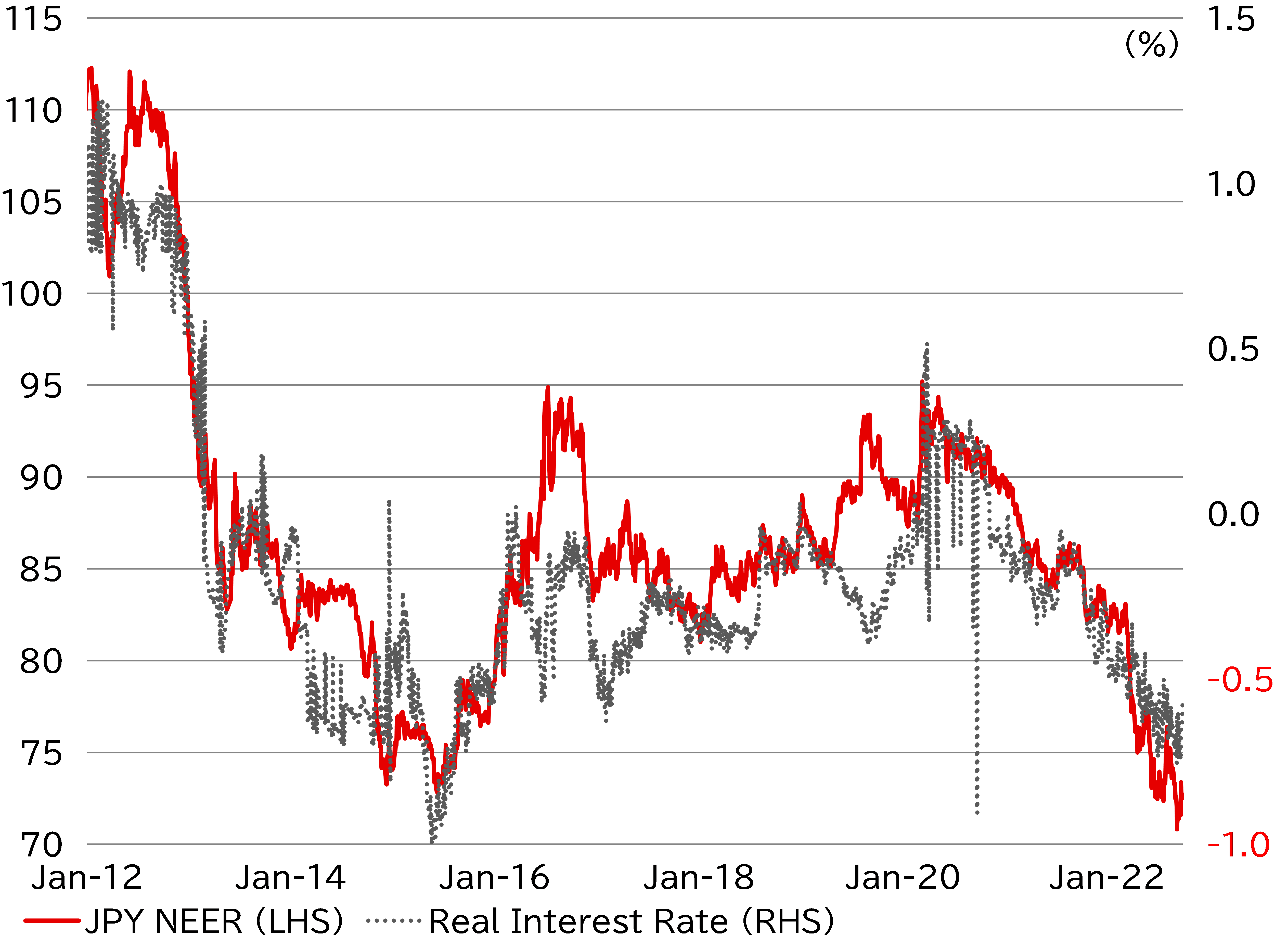

Nominal interest rates are being held down by yield curve control measures and are unlikely to rise, while expected inflation rates should remain elevated. We therefore expect the real interest rate to remain low and see little prospect of a full-fledged shift to a stronger yen in the near term (Figure 5).

In light of this, the next BOJ Governor will probably be tasked with adjusting monetary policy, which currently seems to be aimed at sustaining existing policies themselves. The governor of the Bank is appointed by the Diet and the nomination is likely to be made at the regular Diet session in January. However, expectations of a change in monetary policy could come to the fore again if the name of a specific candidate is revealed. We expect the US to shift to a more accommodative monetary policy stance at this time, meaning that the divergence in monetary policy will narrow from both directions if the BOJ also moves to adjust its policy settings under the new leadership. In other words, the narrowing of the divergence in monetary policy in Japan and overseas could become the theme for next year or next fiscal year. The risk of a rapid decline in the USD/JPY could also emerge.

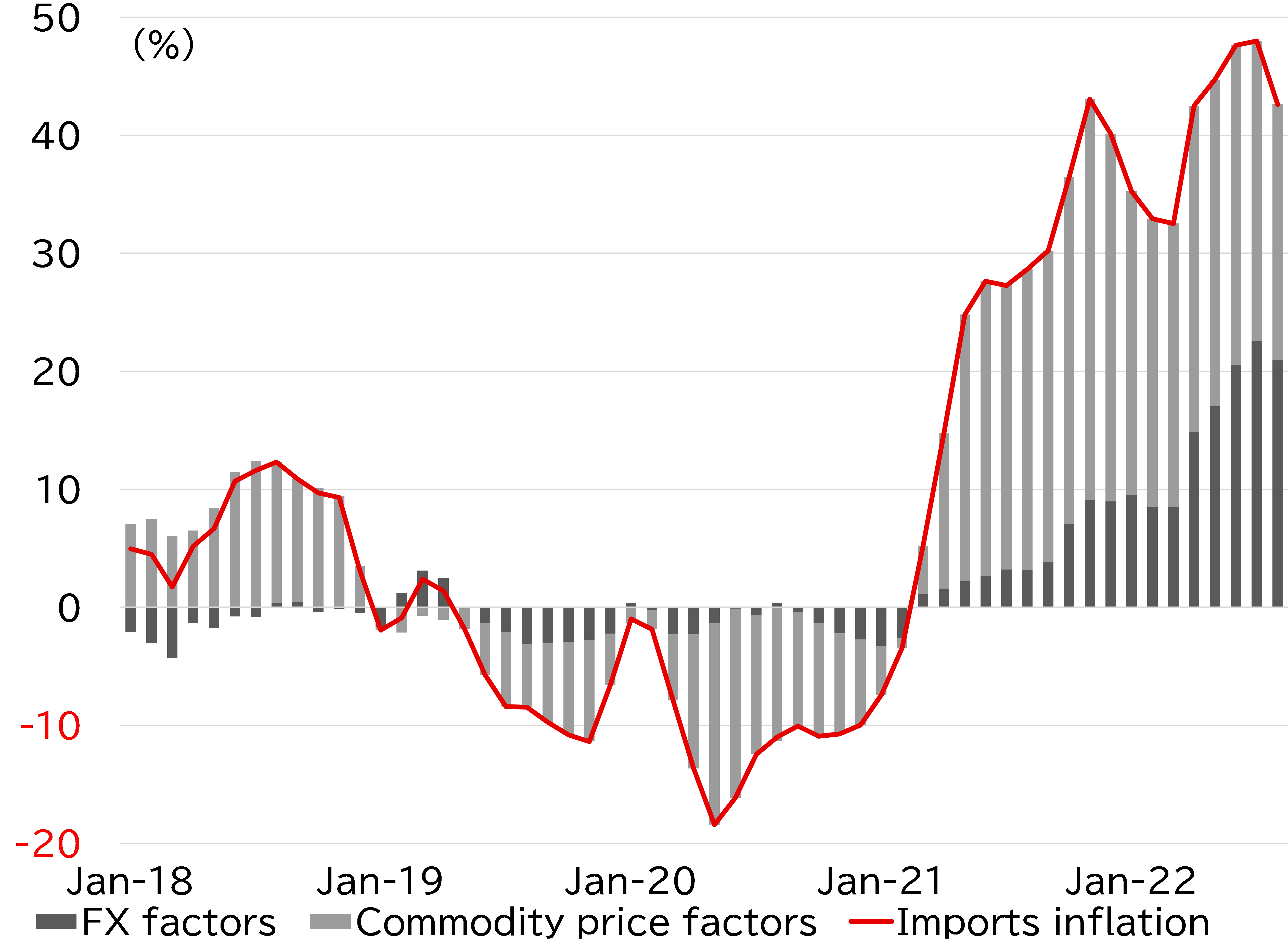

The Japanese government on 30 September announced that it had formulated a package of comprehensive economic measures. Apparently, the main pillars of the package will be a response to the sharp rise in prices and efforts to increase wages. The reason behind rising import prices has recently shifted from commodity prices to the weak yen (Figure 6). It is reasonable to assume that the rise in import prices due to the weak yen will be passed through to consumers despite any measures taken this time. We see the risk that this could increase public dissatisfaction as it has in the US, which could have an impact on monetary policy even before Kuroda's term expires.

FIGURE 5: YEN NEER AND REAL INTEREST RATE

Note: The real interest rate is the 10y JGB yield minus the 5y5y forward inflation swap rate

Source: BIS, Bloomberg, MUFG

FIGURE 6: IMPORT PRICE INDEX (YOY)

Source: BOJ, MUFG

TABLE2: QUARTERLY FORECAST RANGE AND PERIOD-END FORECAST

Our forecast range estimates the high and low for each quarter. The period-end forecast is our forecast for USD/JPY at 17:00 New York time at the end of each quarter.