To read the full report, please download the PDF above.

Reflation supports EMs weather higher DM rates

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

LEE HARDMAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for EMEA

T: +44(0)20 577 1968

E: lee.hardman@uk.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

Macro focus

Global markers are trading reflation, as US data surprises have turned up, global PMIs are strengthening and commodities are surging. An improving global growth outlook helps provide offsets for EM assets to higher US yields. The growth implications should support EM assets which have been reluctant to embrace this driver returning, with commodity prices also rising and providing support. This is an environment which we view as net positive for EM assets, given rates have already repriced and growth is broadening ahead of expectations. Though, we acknowledge that EM bond yields will depend on the path of the Fed which is very data dependent, with another strong US inflation print likely enough for a recalibration.

FX views

Emerging market currencies have rebounded over the past week even as US yields have continued to adjust higher indicating that the USD has lost some upward momentum ahead of the upcoming FOMC meeting. The Fed is expected to deliver a hawkish policy update in the week ahead. We expect Fed Chair Powell to reiterate that the recent run of stronger US activity and inflation data will delay their plans to begin lowering rates into H2 2024.

Week in review

Turkey kept rates on hold at 50.00% and remains in a wait-and-see mode. Hungary slowed the pace of cuts to 50bps to 7.75% with a hawkish stance. Inflation in Saudi Arabia for March edged lower to 1.7% y/y owing to weaker food prices. Abu Dhabi issued USD5bn in international capital markets – first time in 2021. Finally, Egypt delivered a marginal tightening via its 7 day main operation.

Week ahead

In the coming week, there will be monetary policy meeting in the Czech Republic (MUFG and consensus -50bps to 5.25%). Inflation data for April will be released in Turkey (MUFG 70.1% y/y; consensus 70.2% y/y). Finally, Q1 2024 flash GDP estimates for the Czech Republic (MUFG 0.4% y/y; consensus 0.3% y/y) and Hungary (MUFG and consensus 1.3% y/y) will be published.

Forecasts at a glance

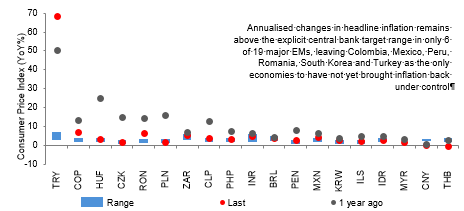

Growth across the EM universe is set to stabilise as domestic fundamentals offset external drags, with some rotation from the largest to smaller EMs. Inflation and interest rates are both “over the hump” – disinflation is progressing, and the decline in rates will continue and broaden in 2024 (see here).

Core indicators

According to the IIF, EM fund flows attracted USD32.7bn of inflows in March – the fifth consecutive month of increases.

Source: Bloomberg, MUFG Research